Three Speculative Microcaps I Own

A quick introduction

The following is a high-level overview of rather speculative microcaps I added to my portfolio.

Please note that these are brief introductory summaries. They are intended solely to outline the core thesis and near-term catalysts. Given the illiquidity and binary nature of these specific setups, strict position sizing and risk management are mandatory.

Disclaimer: I hold positions in the equities mentioned below. This is not financial advice or a recommendation to buy. Always do your own due diligence before deploying capital.

Energous Corporation (WATT)

Price: $13.5

Marketcap: $30m

EV: $19m

LTM Revenue: $5.6m

Energous (WATT) is a microcap technology company that has successfully pivoted from trying to wirelessly charge consumer electronics to powering the rapidly growing “ambient IoT” market. Their core product, PowerBridge, is a fixed-infrastructure wireless power network that continuously emits RF energy to power battery-free sensors. This allows enterprise customers in retail, cold-chain logistics, and distribution to track real-time data like temperature, condition, and location without the massive expense and labor of replacing batteries at scale. By eliminating the battery bottleneck, Energous is helping businesses feed continuous, real-time data into their supply chain analytics and AI models.

The bull case for Energous rests on a massive recent inflection in commercial success. In early 2026, the company pre-announced 2025 revenue of $5.6M (over 600% YoY growth), with $3M generated in Q4 alone. This hyper-growth is being driven by enterprise deployments, heavily hinted to be massive rollouts with Walmart (a “Fortune 10” retailer) and Amazon (a “Fortune 100” tech company integrating via AWS). Despite the recent run in the stock price, the company is poised for steady high growth and a highly positive newsflow throughout 2026 as these Fortune 100 deployments continue to scale and new AWS-partnered customers are onboarded.

However, there are still significant risks and hurdles ahead. Because of the company’s operating costs, a major issue is that Energous will need to scale its revenue significantly, likely hitting $5M to $7M per quarter just to reach profitability, which is still estimated to be 12 to 18 months away. While the balance sheet is being repaired, there is always the lingering risk of further shareholder dilution through their ATM facility to fund the working capital. Additionally, the company faces risks related to heavy customer concentration, the potential for these massive rollout schedules to stall, and the ever-present threat of new competing technologies emerging in the fast-paced IoT sector.

Springbig Holdings (SBIG)

Price: $0.0093

Marketcap: $0.4m

EV: $8.5m

LTM Revenue: $23m

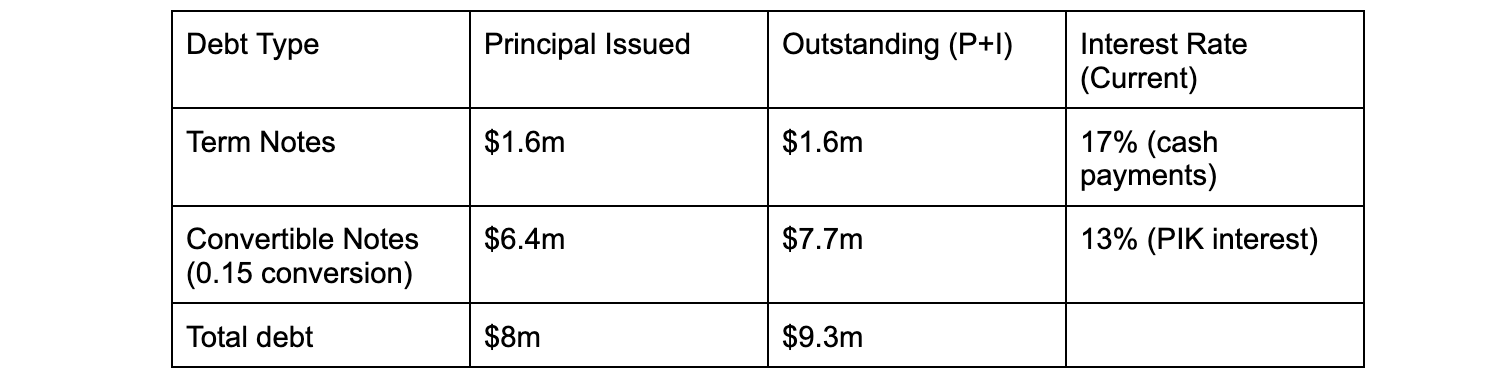

Springbig is a highly speculative, distressed turnaround play in the cannabis software and marketing sector. Once a prominent SaaS platform for dispensary loyalty programs, the stock now trades in the sub-penny range, weighed down by a ~$9.3 million debt wall maturing in January 2027.

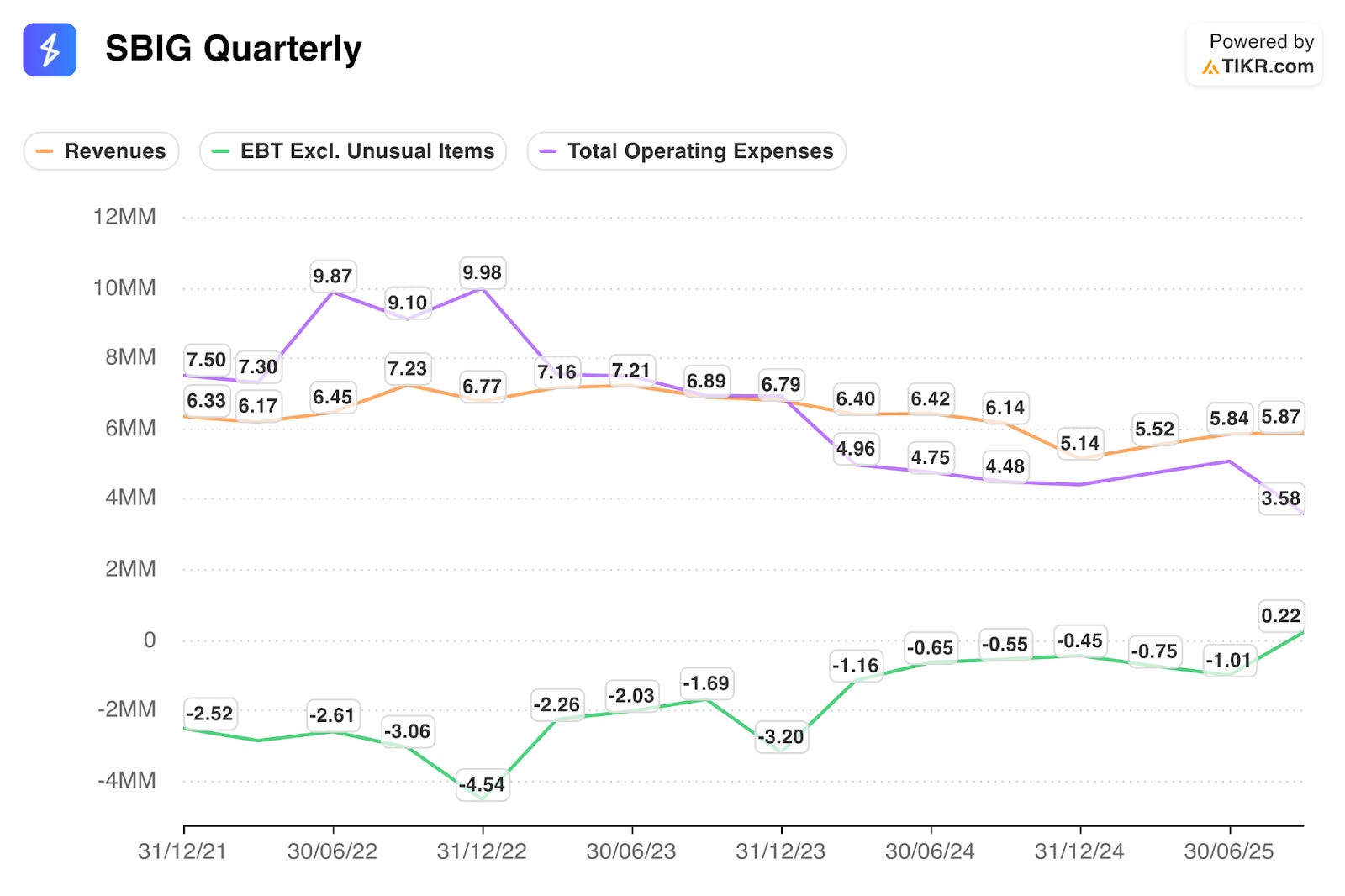

The equity value is down to 0.4m despite having shown pretty good numbers in their latest Q3 report and having around $23m LTM high gross-margin revenue.

Under the new CEO Jaret Christopher, a serial "build-to-sell" founder who previously sold a cannabis CRM to Weedmaps, Springbig has ruthlessly cut costs, pivoted toward AI-driven marketing, and recently posted positive net earnings. If the company can prove sustainable free cash flow, or if the anticipated DEA Schedule III rescheduling revitalizes dispensary software budgets, Springbig becomes a prime, cheap acquisition target for industry consolidators like Alpine IQ or WM Technology (MAPS). For a strategic acquirer, the company is very attractive since they could cut a lot of the overhead costs and get 17 million in additional gross profit.

However, the investment is essentially a ticking clock. If management cannot secure a buyout or refinance the debt before the 2027 maturity, the senior creditors (who recently stepped off the board) are perfectly positioned to force a restructuring or debt-for-equity cram-down. In that scenario, current common equity holders would likely be wiped out entirely. This is a high-stakes, all-or-nothing standoff between management's turnaround efforts and a looming creditor takeover.

Quotemedia Inc. (QMCI)

Price: $0.14

Marketcap: $13m

EV: $16m

LTM Revenue: $20m

QuoteMedia is a B2B financial data provider trading at a deep discount because the market has completely lost faith in its management. For years, CEO Dave Shworan and his team have suffered from a severe credibility gap, characterized by sluggish top-line growth and a frustrating habit of overpromising and underdelivering. Sentiment is virtually nonexistent.

However, looking past the poor investor relations reveals that management’s underlying product strategy was fundamentally correct. Instead of chasing short-term sales, they spent years doing the heavy lifting: securing enterprise-grade SOC 2 Type II compliance and quietly building out their own proprietary data infrastructure. By replacing expensive, variable-rate third-party data feeds with their own fixed-cost infrastructure, they have permanently altered the company’s margin profile.

This creates the primary catalyst the market is currently missing: massive operating leverage. Because their fixed costs are now covered, the incremental cost to deliver data to a new enterprise client is near zero. We saw the first glimpse of this in their recent Q3 results, where they posted a solid 10% year-over-year revenue growth alongside expanding gross margins.

Furthermore, this proprietary data pivot quietly positions them as a “pick and shovel” AI winner. Financial institutions need clean, structured data to train their internal AI models, and QuoteMedia owns and sells exactly that. Management recently launched QuoteMedia Zero (QMZ). This freemium API tier bypasses traditional, expensive exchange licensing fees, creating a brand-new, bottom-up sales channel to onboard startups, developers, and early-stage fintechs.

With management explicitly guiding for several new, larger enterprise contracts launching in Q4, even modest 10% to 15% top-line growth will cause their bottom-line profitability to inflect strongly upward. It is a highly speculative, “show-me” execution play anchored to a heavily criticized CEO, but the asymmetric upside of a proprietary, SOC 2-compliant data provider finally hitting scale is well worth a small position for me.

Nice post! High risk high reward ofc, but interesting picks